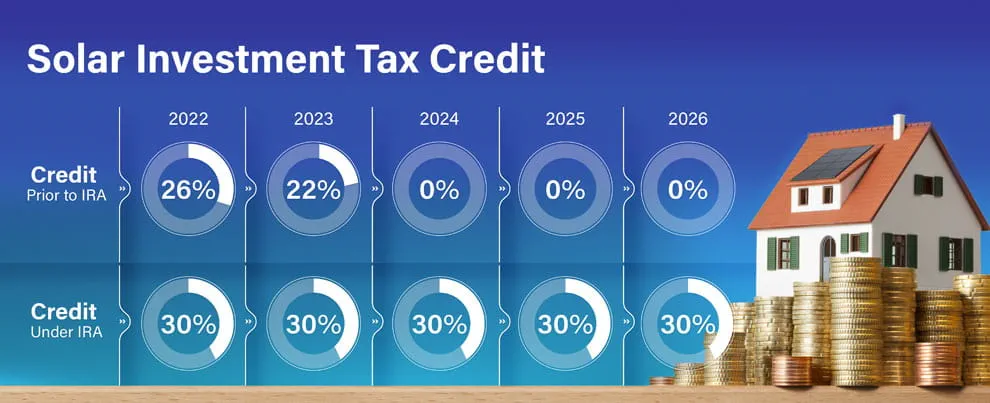

Understanding how federal tax credits work can significantly impact your financial situation. These credits are designed to reduce the amount of tax you owe, potentially leading to substantial savings. In this article, we will explore the intricacies of federal tax credits, their types, benefits, and how to effectively utilize them.

Overview of Federal Tax Credits

Federal tax credits are incentives provided by the government to encourage certain behaviors or activities, such as education, energy efficiency, or investment in low-income housing. They directly reduce your tax liability, making them more beneficial than deductions, which only reduce taxable income. Essentially, a federal tax credit subtracts a specific amount from your total tax bill, thus lowering the overall amount you owe. Understanding how federal tax credits work is crucial for maximizing your tax savings and planning effectively for your finances.

Key Features of Federal Tax Credits

Federal tax credits can be categorized into two main types: refundable and non-refundable. Refundable credits allow taxpayers to receive a refund even if the credit exceeds their tax liability, which means you can get money back if you owe less tax than your credit. Non-refundable credits, on the other hand, can reduce your tax liability to zero but will not result in a refund. Examples of popular federal tax credits include the Earned Income Tax Credit (EITC), Child Tax Credit, and the Education Tax Credits. Each credit has specific eligibility criteria and benefits, making it vital to understand their features when considering how to leverage them.

Benefits and Importance of Federal Tax Credits

The primary benefit of federal tax credits is the direct reduction in tax owed, which can lead to significant financial savings. For instance, a $1,000 tax credit reduces your tax liability by exactly $1,000, unlike a deduction that only reduces taxable income. Additionally, federal tax credits encourage behaviors that can benefit society, such as investing in renewable energy or pursuing higher education. By understanding how federal tax credits work, you can take advantage of these incentives to improve your financial health, invest in your future, and contribute positively to the economy.

Best Practices for Claiming Federal Tax Credits

To effectively claim federal tax credits, maintain accurate records of your income, expenses, and any qualifying activities that may earn you credits. Familiarize yourself with the specific requirements for each credit, as they can vary widely. It’s also advisable to consult with a tax professional or utilize reliable tax software to ensure you maximize your claims and comply with all regulations. Filing your taxes early can also provide additional time to address any issues before the deadline.

Common Misconceptions About Federal Tax Credits

One common misconception is that federal tax credits are only for low-income individuals or families. While many tax credits are targeted at lower-income taxpayers, there are also credits available for middle and higher-income brackets, such as the Lifetime Learning Credit for education expenses. Another misunderstanding is that all credits are refundable; knowing the difference between refundable and non-refundable credits is essential for effective tax planning. By clarifying these misconceptions, taxpayers can better navigate their options and optimize their tax situations.

Cost and Value of Federal Tax Credits

The cost associated with federal tax credits primarily comes from the potential loss of tax revenue for the government. However, the value of these credits to taxpayers can be substantial, often resulting in hundreds or thousands of dollars saved annually. For example, the Child Tax Credit can provide families with up to $2,000 per qualifying child, directly impacting their financial situation. Understanding how federal tax credits work allows taxpayers to recognize their value and strategically plan their finances, potentially leading to long-term savings.

Real-World Applications of Federal Tax Credits

Consider a family with two children who qualifies for the Child Tax Credit and the Earned Income Tax Credit (EITC). By effectively applying these credits, they may significantly reduce their tax liability and even receive a refund. Similarly, a homeowner who makes energy-efficient upgrades may qualify for the Residential Energy Efficient Property Credit, which can help offset the cost of improvements. These real-world examples illustrate how federal tax credits can directly enhance financial situations and incentivize positive actions.

Future Trends in Federal Tax Credits

As the government continues to respond to changing economic conditions and societal needs, future trends in federal tax credits are likely to evolve. We may see an increase in credits aimed at promoting sustainable practices, such as renewable energy adoption and electric vehicle purchases. Additionally, credits may expand to support education and workforce development, especially in high-demand fields. Understanding how federal tax credits work and keeping an eye on these trends can help taxpayers stay ahead and benefit from new opportunities.

Conclusion

In summary, federal tax credits play a critical role in reducing tax liability and encouraging beneficial behaviors among taxpayers. Understanding how federal tax credits work allows individuals to take full advantage of these incentives, resulting in significant financial benefits. By staying informed and proactive, you can maximize your tax savings and contribute positively to your financial health.

FAQs

What are the best practices for claiming federal tax credits?

Keep organized records, understand eligibility requirements, and consider consulting a tax professional or using reliable tax software to maximize your claims.

How does a federal tax credit compare to a tax deduction?

A federal tax credit directly reduces the amount of tax owed, while a tax deduction reduces taxable income, making credits generally more beneficial.

What common mistakes should I avoid when dealing with federal tax credits?

Common mistakes include misunderstanding eligibility requirements, failing to keep accurate records, and overlooking available credits that you may qualify for.

How can I implement federal tax credits in my tax planning?

Stay informed about available credits, maintain thorough records of qualifying expenses, and consult tax professionals to develop a plan that maximizes your benefits.

Are there any resources for learning more about federal tax credits?

Resources such as the IRS website, tax preparation software, and financial advisors can provide valuable information about available federal tax credits and how to claim them.